In building this Web site and incorporating many of my past writings, I have given my best effort to help people become "educated," at least about all the important things that matter about final expense planning, and join the right category. People I meet with regard me as a expert and consultant rather than a "salesman." And the more they themselves know also, the better we get along. The results of about the past seven years with my current offerings is a long list of happy customers (the time period during which I learned how to get you the best plan for your money).

I have become one of the best at a job that hundreds of people have "tried" unsucessfully. Rest assured you won't be meeting with someone trying out a new job or career to see "if it's gonna work." The number of plans I've written over the years is approaching 800.

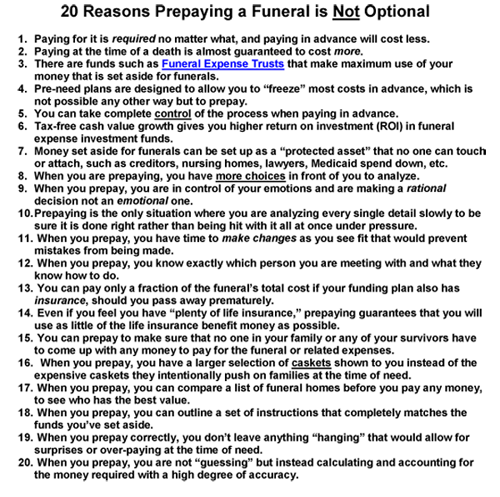

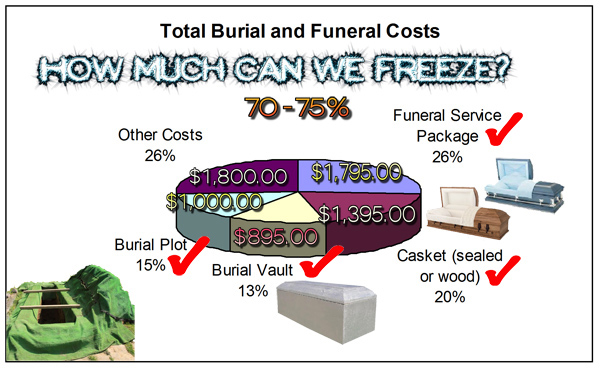

"The key to controlling future funeral and cemetery costs is to arrange and pay for them in advance."

"...people will purchase more in an emotionally charged at-need moment than they will in a calmer and more stable pre-need moment."

"Pre-planning is absolutely the best thing you can do to ensure that you get the final arrangements you want and save money at the same time."

"In my opinion, insurance policies are the best way to go. The insurance industry is highly regulated. Also, insurance companies are typically more balanced and more stable than most death merchants. Even when insurance companies go bankrupt, state and federal agencies come to the rescue of policyholders. Certainly the same cannot be said of funeral homes and cemeteries!"

Internet Resources to Do More Homework

Internet Resources to Do More Homework