Utah Insurance License Number: 88816

Pre-Need Sales Agent Number: 325672-5802

New Information ...

This agency only works with local, privately-owned funeral homes. This means you will be dealing with a trusted member of your community, not some distant corporation only worried about a bottom line.

Click on underlined words for more information.

How to Correctly Use a Church, Reception Center, or Graveside to Save Thousands on a Funeral

The Time to Start Earning Tax-Free Growth is 2017

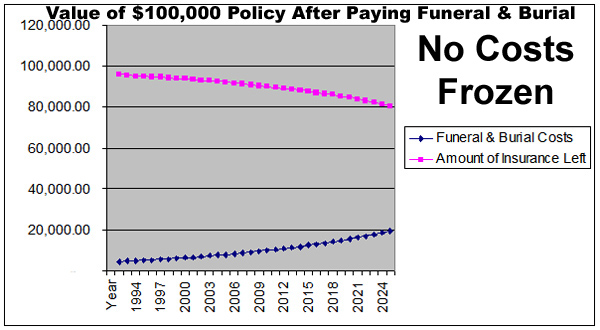

There are ways of PROFITING and getting money back on pre-paid funerals, as well as at-need funerals. But you need to start earning tax-free growth as soon as possible to increase your chances of getting ahead. Freezing your costs is a given when you buy my plans. I have written funeral and burial plans for 25 years. I am going to tell you how to take control of costs but also anticipate some money back with the right funeral provider. You can get money back if you already have a pre-paid plan paid for or underway. You can also anticipate and understand how getting money back is possible if you haven't started a plan yet but know you should start a good funeral plan. If you don't understand what's on this page, a funeral operation can easily gobble up money that belongs to you and your family!

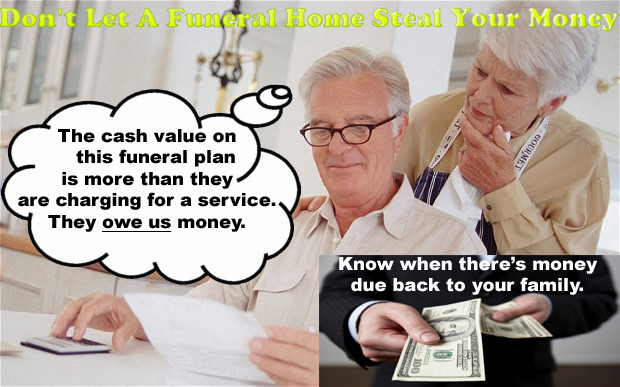

This is not an exaggeration. I have 13 years experience with chain funeral homes. They will keep ALL of the cash value of your plan if your family is ignorant of the facts and the law. The remedy is quite simple. Hold the funeral home accountable. Know exactly how much money is being sent by the insurance company and compare that to the funeral bill. Make them explain it. Better yet: Don't use them. Use a funeral service provider that is honest and that doesn't raise prices very often.

Do you know anyone with a fully or partially paid funeral plan with an expensive funeral home? Convert it to the plan pictured below instead.

Here's how to get a lot of money back. Switch to a funeral service provider such as Premier Funeral Services, Legacy Funerals, Serenity Funeral Home, Holbrook Mortuary, Utah Valley Mortuary, Cannon Mortuary,or other more affordable provider. You simply change the BENEFICIARY of your funds with the insurance company. As long as you have not made the plan "irrevocable" to the first funeral home, this is easy to do. And if the newly chosen funeral home charges only half of what the expensive funeral home does, you can get THOUSANDS back to use more efficiently.

Never "CASH IN" Your Funeral Plan While You're Alive

This is a serious mistake, as it is with most whole life insurance policies that have cash value. Surrendering your plan for cash will net you only a fraction of its true worth. Keep the policy in force until you pass away. At that time, the "death benefit" will be at its maximum. Direct the funds to be used at the best funeral home for the money. This includes "reduced paid up" policies. If you started a funeral plan with a company such as Security National Life but found that it was too expensive to continue, they may have sent you a reduced paid up policy. Keep this with your funeral planning papers. It is worth in cash the amount shown, but only at death.

Don't Let Any Funeral Home Steal Your Cash Value Growth

Funeral plans are normally funded by an insurance company that is specifically in the business of final expense and funeral funding, such as National Guardian Life, Forethought, Great Western, Security National Life, and Homesteader's Life. Funeral homes are only entitled to money at the time of a death up to their interest in the money. Their interest in the money is limited to what they are charging at the time of need for the items specified in the guarantee contract. If the insurance company sends a check to the funeral home that is bigger that what the total charge is for all the guaranteed items, they must refund the difference to the family or apply the excess to other costs--at the discretion of the family.

CRUCIAL: Use a Funeral Home That Doesn't Raise Prices Very Often

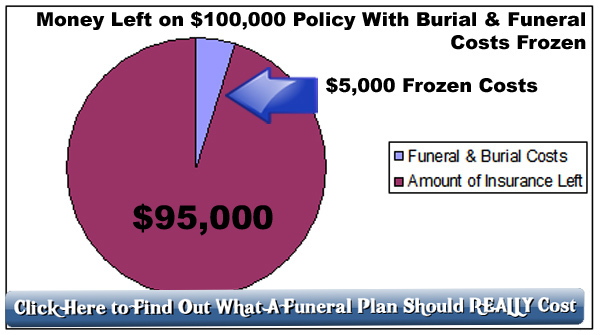

Premier Funeral Services is an example of a funeral home that doesn't raise prices. In fact, in 2015 they lowered prices of a full funeral service from $1,995 to $1,795 and held the line on caskets for the most part. There are some other good funeral homes I like that are reluctant to raise prices: Cannon Mortuary, Holbrook Mortuary, and Legacy Funerals. The high profile and chains don't do this. They raise prices continually to maximize their profit. I explain this on my Web page "Understanding the Funeral Inflation Illusion." Choose a funeral home that doesn't raise prices often, combined with a guarantee contract to freeze your costs, and you can't lose. If they do raise prices, frozen costs remain intact. And again, if the cash value of the plan, the "death benefit," is greater than what they are charging at the time of need, your family is entitled by law to MONEY BACK. See also my page "How to Fully Understand Funeral Plan Guarantees."

Why Life Insurance Alone is Not Enough

If all you rely upon is life insurance, you have no real control. Without the built in guarantees of a funeral plan, the funeral home will charge whatever they want and syphon that from your life insurance policy. There aren't any "checks" you can use whereby you have pre-determined what costs should be. On the other hand, I can set up a pre-paid guaranteed plan that will ensure your total cost for everything will stay in the neighborhood of $5,000 to $6,000--burial plot included. I am going to explain why. Even if you have life insurance, you can ensure that it is used for a better purpose than paying for a funeral, such as providing your survivors with income, paying off debts, etc. Buying life insurance with the sole purpose of paying for a funeral only should be done correctly or it can easily be a waste of money. The best deal of all is to pay cash now, if you have funds, for the guaranteed portion of the funeral. I can do this for you with National Guardian Life and Premier Funeral Services. For example, if you want to freeze the cost of just a casket and funeral service, you can write one check for some discounted amount less than $3,000 and those two things will be set in stone. (Go to my CALCULATOR PAGE to calculate discounts). Not only will you have these two things frozen, your plan will continue to grow in cash value for the rest of your life. Again, this means you could easily have money back.

If you are in a whole life insurance policy now that you bought with the sole intent of paying for a funeral, you need to determine whether it is costing you too much (you will be paying your whole life) and whether it is, in fact, going to be enough. Some people I have met with were in plans that paid only $10,000, with no costs frozen, that were costing as much as $60 a month. And the death benefit is "fixed" at $10,000 with no growth. I can help you determine, if you are paying on a whole life plan, whether it will do what you intended.

In any case, use the guidelines throughout this Web site to ensure you can have the most control possible of what final costs will be. If you are in a situation right now where you can't get any good life insurance due to your health, age, or both, I have guaranteed issue life insurance available to cover funerals as well as other needs. With me, you always get the additional benefit of a professional who can help you nail down funeral costs exactly with the right provider. You don't get this from other life insurance agents. I show you how to be in the driver's seat from the beginning.

No "Surprises" At the End of An Appointment

With most funeral home sales appointments, you are squirming the whole time wondering what the big "surprise" at the end will be: is the payment something you can live with? With me, you already know. I just told you the payments. I use the National Guardian Life Funeral Expense Trust for funding. You can use my calculator page to determine your payment exactly, as well as to determine your "same as cash" or single payment amount. No other funeral home representative does this.

It’s sometimes difficult to ensure a family that “everything will be paid for” with a funeral plan, but it can be built so that it accounts for everything—and very realistically pays for everything. And I can contractually FREEZE your prices of a burial vault, a casket, and a funeral service at today's prices with certain funeral service providers. The rest can be provided for with accurately estimated funds that grow in cash value free of taxation along with the rest of the plan for the remainder of your life. I know how to keep the total cost, even if you make payments, in the neighborhood of $5,000 to $6,000, not $10,000 to $25,000.

Some funeral plans were never intended to pay for everything, and somewhere along the way the message got mixed up. Sometimes a representative will tell the family it will cover “everything” to get the sale. I’ve stumbled across other strange tactics used, such as burial plots that were sold with the promise they could have a funeral service for free at the same facility (an outright lie).

I know how to write a good funeral plan, one that accounts for every cost at prices you want to pay. It can guarantee or freeze many of the costs—depending on what contractual agreement I have with the funeral home. Otherwise, we make reasonable estimates based on inflation and the cash value growth of the funding. Even with higher priced funeral homes, the plans I set up will cost you less than if you fund through them directly.

The more difficult part of guaranteeing that “everything” will be paid for is accounting for cemetery costs, obituary costs, sales tax, and a few other things. These are items that, in the past, have been left out of most funeral plans. This can create a shock at the time of a death, because the total bill for these items today is easily around $2,000 or more. I have practical experience not just with paying for funeral arrangements, I also sold cemetery arrangements for two memorial park operations for a total of 17 years. I can see the whole picture. I do what many representatives don't take the time to do: help you account for everything that is coming and how to lock in the lowest possible cost. When the high profile funeral homes and cemeteries leave things hanging, they are opening the door to hit you with higher costs at the time of need. This does not have to happen to you.

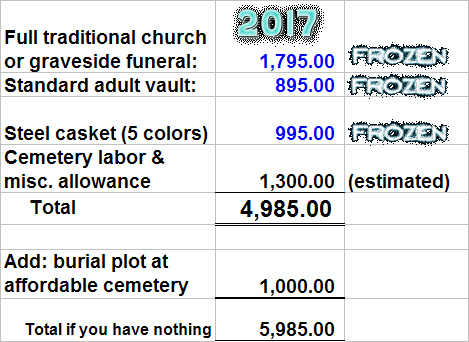

Here's an example of a realistic and feasible plan (summarized) to pay for EVERYTHING for $5,000 or less, with either a payment plan or one payment, through Premier Funeral Services, assuming you already own a burial plot somewhere in the state of Utah. In some cases,a total of $5,500 might be more realistic, but rarely higher than that.

And here's how you can pay for the plan:

All the chains and high profile funeral homes want $6,000+ just for a low end casket and funeral service. Add another $4,000 for the rest: burial plot, vault, cemetery labor, obituary, flowers, taxes, etc., and I think you get the picture. Then if you need to fund it, you're looking at maybe $15,000 to $20,000. Click here to read more about this. Look through my other Web pages on this Web site for more ways to arm yourself against this type of over-spending and getting hoodwinked.

I just completed a survey of what nearly all the Salt Lake County cemeteries are charging for everything. Download it for more information.

If all you have paid for is a burial plot, I can write a $5,000 plan that will more than likely pay for everything you need—if you have a traditional church or graveside funeral service. This will include also the casket, burial vault, and the items shown below. There won't be a surprise bill of $1,000 - $3,000 more for your family to come up with. Note, however, grave marker or headstone is not factored in, because no cemeteries require one, and it can be purchased much later. This is just one example, with a steel casket. A cloth-covered fiberboard casket can be purchased for less (also guaranteed frozen price).

The good news is: with me you don’t have to worry about your family receiving a shocking bill at the time of need. I will make sure you know everything, or nearly everything, that will be paid for with your plan and what costs your family may still be facing. If it is your biggest concern, I make sure your family won’t have to come up with a lot of money. With most plans I write for couples or individuals who want to leave no burdens whatsoever to their families, I show them why the most their family would be facing might be a few hundred dollars. I don’t know future prices of anything, but we can look closely at past inflation and cash value growth of the plan—plus guarantees offered by the funeral home that you get in writing.

If you can’t or don’t need to pre-pay everything, I will make sure all costs are reasonably accounted for.

To take it a step further, so there is no confusion or over-spending, and so that nothing is left out, I do what not very many agents do and create for you a one-page summary called a Final Wishes Summary. This one sheet of paper, after I print it for you or email to you in PDF format, is given to everyone important to you while you are alive. At the time of your death, there is no need for anyone to fish through and sort out a folder or file of papers to see what you have done and what they still need to do. It’s all succinctly on one page, preventing any uncertainty.